The potential of medical electronic data exchange is infinite Traditional electronic data market is saturated

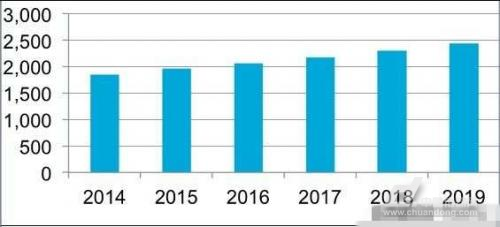

According to the IHS report, global revenue from electronic data interchange (EDI) in the healthcare sector is expected to rise from $180 million in 2014 to over $240 million by 2019. This growth projection comes from the "Medical Electronic Data Interchange Report" by IHS, which highlights a compound annual growth rate (CAGR) of 6% for the medical EDI market. As more healthcare organizations look to improve efficiency in data exchange among suppliers, patients, and payers, the demand for advanced solutions continues to rise.

The medical EDI solution encompasses both software and services, playing a key role in managing, maintaining, and optimizing data transmission between computing systems. The IHS study categorizes medical EDI into four main applications: traditional EDI (such as claims, submissions, and references), patient payments, data analysis, and other optimization services.

The graph above illustrates the growth of global medical data exchange revenue from 2014 to 2019, measured in millions of U.S. dollars.

Implementing an EDI solution streamlines the revenue cycle, reduces the number of rejected requests, and accelerates insurance approvals. To boost efficiency further, more health data is expected to move to the cloud, enabling real-time access for providers, payers, and patients alike.

Andrew Rebhan, an analyst at IHS Medical Healthcare (IT), notes that while the adoption of EDI in healthcare has been slower compared to other industries, it is becoming increasingly essential due to its efficiency and structured approach. EDI helps manage the flow of various types of health data between clinics and health systems, shifting from paper-based to electronic formats that align with EDI standards. However, challenges remain in ensuring timely and accurate data delivery to the right users.

According to the IHS report, patient payments and data analysis have driven the strongest growth in medical EDI applications, particularly in the United States. Rebhan points out that patients are taking on more financial responsibility, including co-pays, co-insurance, and deductibles. This shift has led to increased demand for efficient payment processes, especially in high-deductible health plans. As a result, suppliers must prepare for more transactions involving direct patient payments.

Traditional EDI applications are now reaching market saturation, with most vendors offering some form of EDI functionality. By 2019, the share of traditional EDI in total U.S. revenue is expected to decline, largely due to the rapid growth of patient payment and analysis segments.

Regulatory changes also play a significant role in shaping the medical EDI market. With the implementation of ICD-10, the 10th edition of the International Statistical Classification of Diseases and Related Health Problems, healthcare providers, payers, and IT companies face new compliance requirements. Many providers have struggled with the transition, as the complexity of ICD-10 has delayed full adoption. Rebhan emphasizes that regulatory oversight has placed a heavy burden on the entire claims process, and many suppliers are still unprepared to fully implement the new system this year.

Power Accessories,Steel Wire Tension Clamp,Rubber Insulation Tape,Rubber Arrester

JIANGSU XINJINLEI STEEL INDUSTRY CO.,LTD , https://www.chinasteelpole.com